Intel Q2 2014 Quarterly Earnings Analysis

by Brett Howse on July 15, 2014 7:55 PM EST- Posted in

- Intel

- Smartphones

- Mobile

- Datacenter

- desktops

- Notebooks

On July 15, Intel released their Q2 2014 Earnings report for the period ending June 28, 2014.

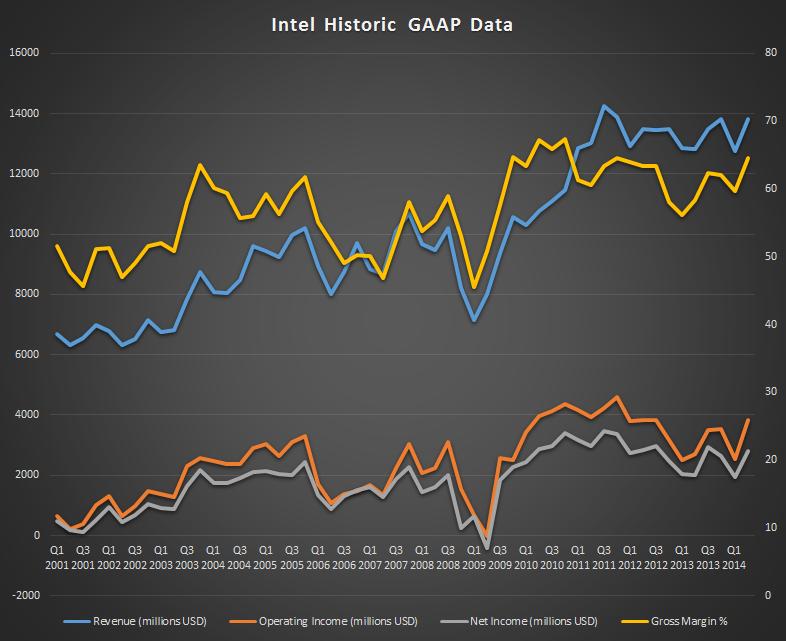

GAAP revenues for the quarter came in at $13.8B which is up almost a billion over Q1 2014, and also up a billion on Q2 2013 for a strong 8% increase.

Earnings Per Share was $0.55, up a substantial 41% year-over-year, and beating analysts’ expectations of 52 cents per share.

| Intel Q2 2014 Financial Results (GAAP) | |||||

| Q2'2014 | Q1'2014 | Q2'2013 | |||

| Revenue | $13.831B | $12.764B | $12.811 | ||

| Operating Income | $3.844B | $2.533B | $2.719B | ||

| Net Income | $2.796B | $1.947B | $2.000B | ||

| Gross Margin | 64.5% | 59.7% | 58.3% | ||

| PC Group Revenue | $8.7B | +9% | +6% | ||

| Data Center Group Revenue | $3.5B | +14% | +19% | ||

| Internet of Things Revenue | $539M | +12% | +24% | ||

| Mobile Group Revenue | $51M | -67% | -83% | ||

| Software and Services Revenue | $548M | -1% | +3% | ||

| All Other Revenue | $517M | -5% | +16% | ||

The stagnant PC sector is finally showing some signs of life again after declining over the last several years. Intel’s PC Client Group reported revenue of $8.7 billion, up 9% over last quarter and 6% year-over-year. Unit volumes of PC Client chips were up 12% over last quarter, and 9% from last year. The average selling prices (ASP) were down 3% from Q1 2014 and 4% from Q2 2013. Most of this can be attributed to a 7% drop in ASP for the notebook platform, where as desktop chips actually slightly increased ASP over Q2 2013.

Data Center revenue was up an even more impressive 19% over Q2 2013, and 14% over last quarter. Data Center volumes were up exactly the same as the PC Client volumes – 12% over the previous quarter and 9% over the previous year, but ASP for the Data Center platforms was up 3% over Q1 2014 and 11% over Q2 2014.

The recently formed “Internet of Things” group continued its strong growth, up again another 12% over last quarter and 24% year-over-year. This group includes embedded segments such as retail, transportation, and consumer focused things like home automation.

The one sector at Intel which continues to struggle is the Mobile and Communications group which was down 61% Q1 2014 versus Q1 2013, and once again in Q2 2014 it was down again 67% compared to Q1 and 83% year-over-year. The silver lining on this is the relatively small amount of revenue this is for Intel with this group only having $51 million in revenue, but in a world where the number of mobile devices is skyrocketing, Intel is struggling to capitalize on the new market. Intel is still not price competitive with the Bay Trail SoC business and are working on a low cost platform for Bay Trail. In the meantime, Intel is subsidizing the platform cost for the time being in order to not be shut out of this market. It’s not something that would be sustainable forever, but it seems to be allowing them a toehold in the mobile market while they continue to push towards lower cost silicon for partners. We’ve seen a lot of mobile devices coming with Bay Trail in the last couple of months, including a $110 Toshiba tablet and this contra revenue is driving that, but hurting the short term results for the Mobile group.

The last sector at Intel to report was the Software and Services, coming in at $548 million in revenue which is pretty much flat quarter-over-quarter and year-over-year. This segment includes McAfee which was purchased by Intel in the not so distant past.

The forecast for next quarter and the rest of the year has been upgraded, with Q3 2014 being forecast for $14.4 billion plus or minus $500 million. The board has also approved an additional $20 billion in share repurchases, with an expectation of $4 billion in shares to be repurchased in Q3. Looking back historically, Intel is once again getting close to record revenue and incomes, having almost fully recovered to 2012 levels.

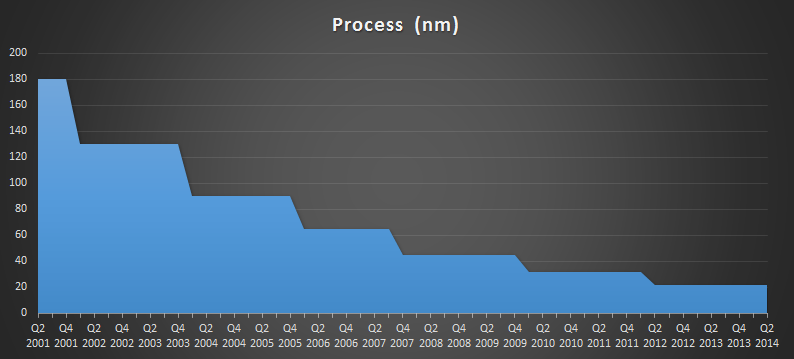

Broadwell is now expected during the holiday season 2014, which is certainly much later than hoped. Going back to 130 nm and coming forward until 32 nm, Intel has averaged 8.2 quarters between process nodes. They have been on 22 nm for nine quarters already, meaning the wait between 22 nm and 14 nm will be about 11 quarters which will be the longest time on a single process node since Intel began the tick tock strategy. Clearly there are some heavy engineering hurdles to overcome as we move towards smaller and smaller processes. We’ll have to watch and see if this delays Skylake or if Broadwell has a shorter than expected lifespan. 10 nm is on the roadmap for 2016 which might be an aggressive timeline with the time 14 nm has taken.

This was a great quarter for Intel, which is generally a bellwether for the rest of the PC industry. After several years of decline, things are looking more optimistic for the industry. Revenues from Intel were great, but historically they have always done well. The exciting takeaway from this earnings report is the increased volumes in both notebook and desktop sales. Whether this is a turnaround in the market, or just a small correction is tough to tell yet.

Source: Intel

33 Comments

View All Comments

name99 - Wednesday, July 16, 2014 - link

You are conflating a whole lot of separate markets as a single "desktop" market.There are special-purpose devices (like ATMs, cash registers, industrial control machines). No-one cares about these --- they can run off the cheapest Atom, and they run until they die. They're not going to keep Intel rich.

There are ENTERPRISE desktops. These think they need to run Office and some PoS customized app written in Visual Basic in 1997 and never updated since then. THAT is when Intel and MS have a lock.

There are HOME desktops (to a large extent this also includes schools and colleges and small businesses). These are much more flexible in what they run, and don't care about the details as long as they get functionality -- they want word processing, not Word, or Browsing, not IE. We are already seeing this space fragment. This is where Apple, of course, lives. But also Chromebooks (to the extent they are sold) and plenty of iOS and Android activity in varying form factors. All this activity makes Wintel compatibility just not that valuable.

So basically Wintel has one lockin, the enterprise. This is a valuable lockin, but it's not massively growing; on the contrary it gets nibbled at every day. The Apple/IBM alliance announced yesterday is one more part in this nibbling. It's a small part (for now) but sets the tone.

Part of MS' problem is that we now have a pretty good model, which covers a large number of use cases, for how to replace that software written in 1998 --- have the backend serve up HTML which gets displayed either in a web browser or some sort of mobile wrapper app. I expect many of the IBM replacement mobile apps they talk about to be written that way, and every one that does is a further proof of concept.

This doesn't help a few specialized cases (people who push Excel hard, a very limited market; people who use Office VB macros to design an enterprise workflow, a rather larger market) but it means Wintel SW lockin is fighting an ongoing battle, and losing a little every month.

Speedfriend - Wednesday, July 16, 2014 - link

@TheJianARM marches on desktops - what a joke, the fastest ARM chips barely outperform an Atom and no-one is suggesting putting them in a desktop. It is more likely Intel eats Arm at the higher end of mobile with Broadwell than Arm eats Intel in desktop.

Look at what the market is telling you, since March Intel is up 23% while ARM is down 19%.

Giving away 40m tablet chips is the right strategy, once people try a Wintel tablet, they are not going to go back to some crappy android tablet. Even my iPad Air is barely used for anything other than surfing the web or watching movies. Trying to do anything productive on it is like slamming your head against a wall.

name99 - Wednesday, July 16, 2014 - link

"ARM marches on desktops - what a joke, the fastest ARM chips barely outperform an Atom and no-one is suggesting putting them in a desktop."The fastest ARM chip is Apple A7. This performs equivalent to an i3/i5/i7 at equivalent GHz.

iPad Air has an A7 at 1.4GHz. MBA has an i5 at 1.6GHz. MBA feels faster because the i5 turbos up to 2.4GHz, and Intel turbo'ing is so good that it can run most "snappy" UI stuff at the 2.4GHz.

There is every reason to expect that A8 will run at same IPC but clocked at 2GHz.

A6 was a 2x speedboost over A5. (about 1.6 from process, 1.2 from micro-architecture)

A7 was a 1.5x speedboost, all micro-architecture. I'd expect A8 to be about a 1.5x speedboost, about 1.4x from process and 1.1 from micro-architecture).

In the six years since Nehalem, Intel has sped up by about 1.25x, all microarchitecture since all their process has been used in lowering power. (This is not quite true, and is especially misleading in the Y category, because turboing has been used to give substantial frequency boosts to nominally low frequency ULV processors).

OK, that's the state of the art today. Extrapolating to the future, the patterns that matter are

- Apple is vastly more agile than Intel. This is primarily because they don't have the baggage of 30+ years of accumulated poor ideas that have been added to the x86, none of which have ever been removed.

- Apple has had it easy so far, especially in improving micro-architecture, because they have been playing catchup. There is not much scope for improvement there as long as they stick to conventional micro-architecture. BUT there is also no reason that they have to stick to conventional micro-architecture. They aren't Intel, terrified of change and with an unbelievable test burden. They are in a better position than anyone else to experiment with an unconventional micro-architecture like kilo-insruction processing, which could net them another 30% or so.

- Apple have managed to match Intel with a core that is smaller (100mm^2 for the ENTIRE A7, about 35% of which is stuff that's not CPU or GPU), cheaper to make, on a lower process. The ARM hoard will catch up to this point eventually. They can ALSO move faster than Apple, and they will be more aggressive given that Apple has shown proof of concept.

- There seems no intrinsic reason why Apple cannot, over the next three or four years, copy the parts of Intel that matter and which they are missing to reach parity. More cores is trivial. Higher frequency is primarily a question of how much power you're willing to burn. If Apple wanted, they could copy AVX2 and go with wider vectors, but I think they see HSA as more promising way to solve that problem. Better uncore (NoC, common NUCA-based L3, etc) are coming soon, I expect in the A8. HW transactional memory is coming soon, I also expect in the A8.

The issue is NOT that Intel is ahead today. The issue is that

- Intel is less agile

- Intel has no compelling technical advantages

- Intel cannot survive on the cost structure that the ARM ecosystem is used to.

Intel won't be replaced on the desktop tomorrow. But in five years...?

Speedfriend - Thursday, July 17, 2014 - link

"The fastest ARM chip is Apple A7. This performs equivalent to an i3/i5/i7 at equivalent GHz."No, an i7 at 1.4ghz, using only 2 cores scores half the A7 time on sunspider.

There is also no evidence of the A7's ability to be clocked to anywhere near the level that the i5/i7 run at.

From all accounts, the A7 is way behind Haswell on a performance per watt basis.

There is far more evidence that Intel is moving down the power consumption curve towards Apple than Apple moving up the processor power curve.

chizow - Tuesday, July 15, 2014 - link

Not surprising in the least, I just realized a few days ago that I had purchased 4 Haswell-based products over the last year (2x4770K desktop builds, 1xNUC, 1xSurface Pro 3). Intel really did an amazing job scaling this architecture for all work loads while maintaining high performance and full x86 Windows compatibility.I think we will see more of this in the future and this was the first quarter where the market came to the same realization that I did over a year ago. I'm done with the novelty of all these gadgets running toy OSes like Android and iOS, when it comes down to business, gaming and productivity, there's just no replacing a full blown x86 ISA chip running full blown Windows. As much as Win8/.1 are maligned, it's really a better OS after you get past the fullscreen Modern UI (which is thankfully going away with Threshold).

mkozakewich - Wednesday, July 16, 2014 - link

To be fair, there's no reason Windows can't run as well on an ARM chip. There's just the matter of older software, but anything new could be cross-compiled if Microsoft allowed binary executables on the Win8 desktop.I completely agree with you on Windows, though. I simply couldn't have a productivity machine that uses Android or iOS. People have debated between the interfaces between OSX and Windows for years; but when you bring the argument to things like Android, Windows wins hands-down. It's just a lot easier to use.

jjj - Wednesday, July 16, 2014 - link

According to everybody, Intel included, the refresh in business PCs caused by XP's EOL is driving sales but consumer is still soft. So not much of a good news since it's a temporary thing and lets face it ,the worst is still to come for them. For now other devices have made the traditional PC less relevant but those new devices will start to replace PCs at some point - it should have started already but the mobile players don't seem too interested.14nm is in theory arriving late this year but it seems very low volume and a proper roll out will be over the first half of next year.

10nm might have to come rather fast or the foundries might catch up, things are heating up there and chances are TSMC and Samsung will be racing each other hard.

Hope AMD's new cores will be competitive because this lack of competition is just allowing Intel to offer less and less, else at some point soon they'll start selling us mobile SoCs sized chips at 300$, just because they can.

stadisticado - Wednesday, July 16, 2014 - link

Do you mean sized or powered? As it is, baytrail is ~100mm2. Haswell is north of 175mm2. As gfx becomes more and more prominent that gap is going to narrow, especially as Atom and Core start using the same gfx subsystems. As for power, that will also narrow a lot. My speculation is that fanless Broadwell and Skylake will maybe, maybe be 25% faster on the CPU side than Cherrytrail/Broxton. That's simply due to a TDP limitation.errorr - Wednesday, July 16, 2014 - link

ARM isn't a danger in desktops because desktops are slowly being marginalized. The only desktop like comps that are worth anything will be workstation grade stuff when you need the heavy lifting a Intel chip will give you.Intel is in no danger of becoming irrelevant as worst thing that could happen is they become the worlds most profitable fab company even if TSMC or Samsung catch up. As long as the barrier to entry for foundries is approaching $10b they won't have a level of competition to eat away their revenues for a while.

Long term I'm also not so sure how profitable mobile chips will be as a segment. The value is all in the fab and chip design is becoming commoditized with the fabless semi companies. When 3g is no longer necessary for modems Qualcomm loses their biggest leverage and their margins will drop.

Intel will need to worry about the server market which has been and will be their cash cow, mobile will be a plus but margins will fall and hurt the stock if they try and compete to heavily in mobile.

If Otenelli had taken the margin hit by fully committing to mobile first before he retired things might be different but that ship has sailed and the new CEO may not have the job security necessary to lose that much money by foregoing xeons for mobile.

Remember AMD hot killed because everyone expected them to make Intel sized margins and they just couldnt because Intel was the outlier and only in retrospect do people realize that AMD tossed their most important asset by splitting with GloFo. The most valuable asset AMD has left is their cross licensing deal with Intel from the 64 bit transition that allows them to use Intel x86 IP and kept the feds from opening an antitrust case against Intel.

The future is unwritten but Intel will be fine but not the dominant player it once was.

Hrel - Wednesday, July 16, 2014 - link

We need competition so badly... those margins are insane.